Grocery Store Alcohol Sales and Market Shifts

Grocery store alcohol sales have expanded rapidly over the past decade. Legislative changes in states like Colorado, New York, and California opened the door to large-scale retail participation. As a result, national box stores and supermarkets gained significant market share in the off-premise alcohol sector.

Consumers are drawn to convenience and pricing. A single shopping trip allows them to buy groceries and alcohol together. Large chains, meanwhile, deploy deep discounting on top-selling national brands to attract shoppers.

This shift has changed the competitive balance. Independent liquor stores and craft producers face growing financial strain.

The Role of Grocery and Chain Stores in Liquor Sales

Grocery stores and chain retailers have become indispensable in modern shopping. Consumers depend on them for convenience, competitive pricing, and broad product availability. Most of us shop these outlets weekly, and their growing participation in alcohol sales is a natural extension of consumer demand. For many households, purchasing spirits alongside food and household staples simply makes sense.

However, these outlets remain poorly suited to the specialized nature of the liquor industry. Shelf sets are determined by national category managers, not by local preferences or staff expertise. Shoppers encounter rows of large national brands, while smaller craft spirits are often excluded. Unlike dedicated liquor stores, grocery chains rarely provide knowledgeable staff who can guide customers through flavor profiles, production methods, or brand stories.

The result is a retail environment that prioritizes efficiency and volume over discovery and education. While chain stores meet the needs of busy consumers, they cannot replicate the curated experience offered by independent liquor retailers. This misalignment places craft distillers at a disadvantage, limiting exposure in the very channels where sales are growing fastest.

The Squeeze on Independent Liquor Stores

Independent liquor stores traditionally thrived by offering variety and expertise. However, grocery stores and box chains now dominate shelf space. Their pricing power is unmatched, often offering spirits at margins small retailers cannot match.

Data from NielsenIQ shows that grocery and mass retailers account for more than 45% of U.S. off-premise alcohol sales in 2024. Specialty liquor stores, once dominant, now represent less than half the market share they held in the early 2000s.

This consolidation places pressure on smaller retailers. Many face closure as revenues shift toward multi-state retail operators.

Impact on Craft Distilleries

Craft distilleries depend on local liquor stores to showcase unique offerings. When those outlets decline, craft brands lose critical access to consumers.

Chains rarely stock smaller brands. Instead, they prioritize fast-moving national spirits with broad consumer recognition. As a result, consumer choice narrows even further.

The Distilled Spirits Council of the United States (DISCUS) reported that over 30% of craft distillers cite retail consolidation as their biggest sales challenge in 2024. For many, distributor relationships provide little relief, since distributors also prefer brands that sell at scale.

Distributor Bottleneck

The number of distributors in most U.S. states remains relatively fixed. Meanwhile, the number of distilleries has grown sharply since the early 2000s. This imbalance means many small brands cannot secure distribution deals.

According to DISCUS, there are now over 2,700 active craft distilleries in the U.S., compared to fewer than 400 two decades ago. Yet, distributor networks have not expanded proportionally. This mismatch forces more producers to compete for fewer viable retail outlets.

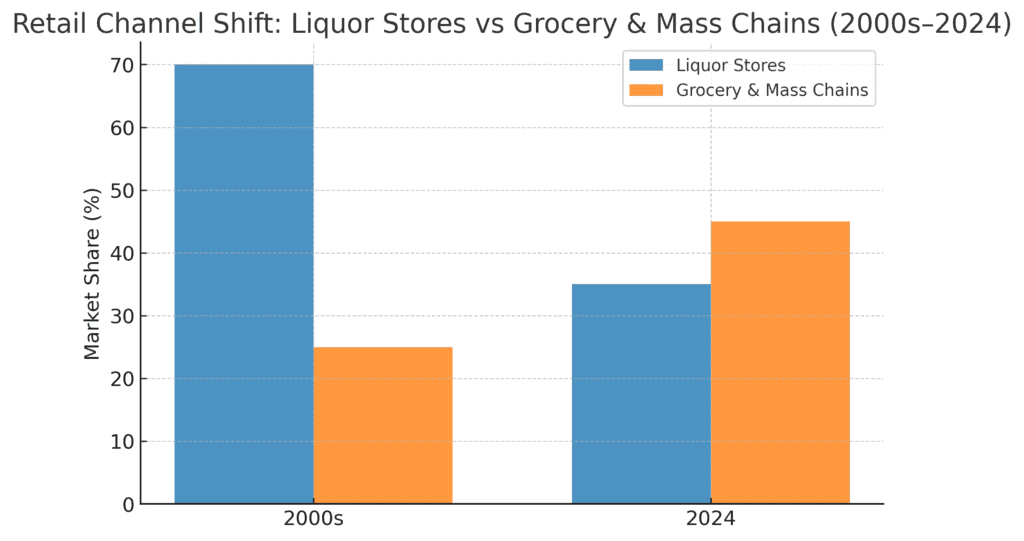

Visualization: Off-Premise Alcohol Sales by Channel

Below is a bar chart comparing grocery/box store alcohol sales versus liquor store sales over time.

Liquor stores once controlled about 70% of alcohol retail sales in the early 2000s. By 2024, their share had fallen to 35%, a dramatic decline that reflects industry consolidation and shifting consumer buying habits. At the same time, grocery and mass chains expanded their role from 25% to 45% of total sales. The remaining market share belongs to convenience stores, warehouse clubs, and emerging online/direct channels. This structural change has created intense distribution challenges for craft distillers, who increasingly find themselves squeezed out of the largest retail segments that favor established national brands.

Consumer Consequences

Consumers ultimately feel the effect. On the surface, grocery store alcohol sales provide lower prices and easier access. However, the trade-off is reduced choice. Craft spirits, local innovations, and niche imports rarely find space on chain shelves.

The long-term risk is homogenization. If craft producers disappear, consumers will find fewer unique products and less innovation in the marketplace.

Fighting for the Future: Why Proposition 125 Must Be Repealed to Save Colorado’s Craft Spirits

Lessons From a Costly Political Defeat

The passage of Proposition 125 in Colorado marked a turning point for local distillers, independent retailers, and consumers. By allowing grocery and box stores to sell wine—and setting the stage for further encroachment into spirits—the law tilted the playing field toward large national brands. The result was predictable: consolidation of shelf space, declining revenue for specialty liquor stores, and mounting pressure on craft distilleries already struggling with thinner margins.

The problem was not only the law itself but also the way it passed. Industry lobbying groups divided their attention among three ballot measures: Proposition 124 (license expansion for store operators), Proposition 125 (wine sales in grocery stores), and Proposition 126 (delivery regulation changes). Instead of focusing resources on the existential threat—Proposition 125—efforts were diluted by the special interests of a handful of large retailers.

Producers warned against this lack of focus. They urged the lobbying coalition to prioritize the grocery store issue and avoid distractions tied to delivery rights or expanded chain licenses. Their advice was ignored. The result was the loss of two out of three ballot measures, including the one that mattered most.

Fallout and Retribution

The lobbying missteps were compounded by the aftermath. Rather than acknowledging the failure, some influential retailers turned against local producers who had sounded the alarm. Blacklists were created, local products were removed from shelves, and slogans like “Keep Colorado Local” were used even as consumer choice shrank.

Ironically, the strategy backfired. Consumers demonstrated strong demand for local spirits, and independent store owners who embraced Colorado-made products saw higher margins and stronger customer loyalty. The punitive tactics weakened trust, deepened divisions, and left independent retailers without the unity they needed to resist consolidation.

Why Proposition 125 Must Be Repealed

The continued presence of Proposition 125 threatens the long-term health of Colorado’s independent spirits ecosystem. If grocery and box stores are allowed to expand alcohol sales unchecked, specialty liquor stores will continue to close. As they disappear, craft distilleries lose critical retail partners. Eventually, consumers will find themselves limited to the same handful of national brands, stripped of the diversity that once defined Colorado’s spirits scene.

Repealing Proposition 125 is not just a fight for local producers; it is a fight for consumer choice, small business sustainability, and Colorado’s cultural identity. Without action, the consolidation spiral will continue until independent voices are silenced.

Building a Smarter Coalition

The mistakes of the past offer clear lessons for the future:

- Focus on the Core Threat: Resources must be concentrated on fighting laws that directly undermine consumer access to local products.

- Unite Producers and Independent Retailers: Special interests cannot drive the agenda. The majority of store owners and distillers must stand together.

- Educate Voters: Clear messaging about consumer choice, local jobs, and community identity resonates more than abstract license or delivery debates.

- Promote Transparency: Efforts must avoid backroom politics that alienate producers. Open communication builds trust and unity.

A Call to Action

Colorado’s spirits industry faces a crossroads. Repealing Proposition 125 will require organization, focus, and a willingness to learn from past mistakes. The coalition that emerges must represent the true interests of small businesses and consumers—not the narrow goals of a few large operators.

The fight is not only about keeping shelves diverse; it is about preserving a way of life that values entrepreneurship, community, and innovation. If independent producers and retailers come together with a focused strategy, Proposition 125 can be undone. The alternative is a market dominated by national chains, where local craft spirits are relegated to the margins.

Now is the time to choose the future of Colorado’s craft distilling industry.

Industry Outlook

The liquor industry is entering a contraction phase. Sales volume of spirits in the U.S. has shown signs of slowing since 2021, following two decades of steady growth. At the same time, operational costs for craft distilleries have risen.

Retail consolidation accelerates this cycle. Unless states intervene to preserve liquor store independence, or unless new direct-to-consumer channels expand, craft producers will remain squeezed.

The question is not whether grocery store alcohol sales will grow further. The question is how many independent players will survive.