Grocery store alcohol competition has accelerated over the past five years, reshaping liquor store sales, margins, and long-term viability. Large grocery chains now use scale and buying power to underprice high-volume spirits, drawing traffic away from independent liquor stores. As a result, core revenue streams that once funded selection, staff expertise, and product discovery have weakened.

This article examines five years of data, explains the structural causes, and outlines what comes next.

The core issue, stated clearly

Grocery chains compete on alcohol using buying power, not expertise. They focus on high-volume national brands and price leadership. As a result, liquor stores lose core revenue that supports staff, selection, and discovery. Over time, fewer stores survive. Consumers then face fewer choices. Craft producers also struggle to gain shelf access.

Grocery Store Alcohol Competition Over the Past Five Years

From 2021 through 2025, grocery retailers increased alcohol shelf space across many states. At the same time, lawmakers expanded grocery privileges, often starting with beer and wine. Colorado offers a clear example.

In 2019, Colorado allowed full-strength beer in grocery stores. In 2022, voters approved grocery wine sales. Large chains rolled out wine programs in 2023. Soon after, lawmakers responded to retailer concerns and limited further expansion in 2025.

This pattern repeats nationally. Convenience expands first. Market impact follows. Policy correction comes later.

RELATED: How to Increase Liquor Store Profits

How Grocery Store Alcohol Competition Pressures Liquor Store Margins

National retail sales data helps separate growth from channel shift. According to U.S. Census data published through FRED, liquor store sales surged during the pandemic. Growth then slowed. Grocery sales also grew, but from a far larger base. Grocery store alcohol competition concentrates pricing power in a few national chains, forcing liquor stores to defend shrinking margins.

When indexed to 2019, liquor stores grew faster early. However, grocery stores steadily closed the gap by 2025 on a year-to-date basis. Grocery growth now matches or exceeds liquor store growth in several recent periods.

This trend matters. Grocery chains already control far more total retail spend. Even modest share gains translate into major dollar shifts.

According to U.S. Census retail sales data published via FRED, grocery store sales growth steadily closed the gap with liquor stores between 2019 and 2025.

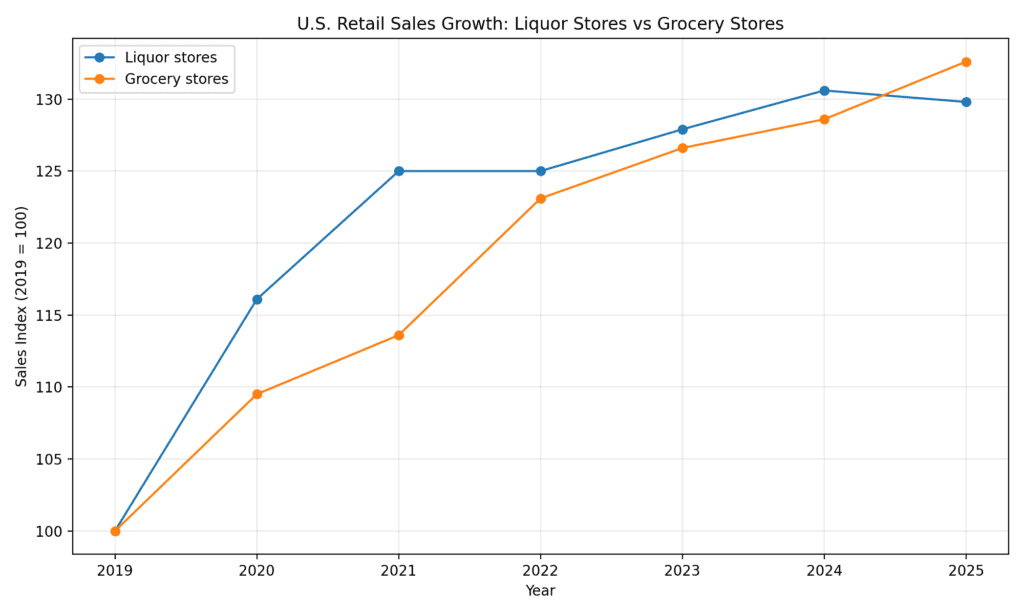

What the Retail Sales Chart Reveals About Grocery Store Alcohol Competition

The chart compares U.S. retail sales growth for liquor stores and grocery stores from 2019 through 2025. Both lines use an index where 2019 equals 100. This approach removes scale distortion and allows true growth comparison between channels.

Liquor stores showed faster growth during 2020 and 2021. Pandemic buying and temporary channel shifts drove that surge. However, grocery store sales grew steadily across the entire period. By 2024 and 2025, grocery growth matched or exceeded liquor store growth on a year-to-date basis.

This convergence matters. Grocery store alcohol competition does not require grocery dominance to cause harm. Even small share gains shift billions of dollars away from specialty retailers. Grocery chains already control customer traffic. Alcohol becomes an add-on purchase, not a destination category.

Liquor stores depend on high-volume national brands to fund staffing, selection, and service. As those brands migrate to grocery shelves, store economics weaken. The chart explains why many liquor stores feel pressure despite stable overall demand.

For policymakers and industry stakeholders, the chart signals structural change, not short-term volatility. Growth continues, but it shifts channels. That distinction explains why states revisit alcohol policy after expansion and why consolidation accelerates.

This visual anchors the discussion of grocery store alcohol competition in measurable data. It shows why scale, pricing power, and access matter more than consumption trends alone.

Why liquor stores feel squeezed despite stable demand

Liquor stores rely on a specific revenue mix. High-volume national brands drive traffic and cash flow. Trade-up items and discovery drive margin. Grocery chains target the first category aggressively.

As those staples move to grocery shelves, liquor stores must rely more on premium and niche sales. That shift raises labor costs per sale. It also increases risk during slow demand cycles.

A store can appear busy while earning less profit. Smaller baskets, deeper discounts, and promo pressure create that outcome.

Why grocery shelves favor national brands

Grocery retail rewards simplicity and speed. Chains prefer tight planograms, fast turns, and strong vendor support. National brands deliver those traits consistently. Craft brands often cannot.

As a result, grocery alcohol sets look similar across markets. They favor proven sellers and avoid risk. This approach limits choice and reduces trial for new producers.

Liquor stores historically filled that gap. As they weaken, fewer outlets support new brands.

Why alcohol retail requires expertise

Alcohol is not a basic commodity. It involves taste, occasion, and risk. Many buyers want help choosing the right product. Liquor stores train staff for that role. Grocery chains rarely do.

In many grocery stores, alcohol receives limited attention. Staff may lack product knowledge. Some employees cannot legally discuss alcohol. The shopping experience then centers on price, not fit.

That shift narrows consumer choice. It also weakens brand education.

A clear industry opinion

Grocery alcohol expansion harms long-term competition. Price leadership removes the revenue base that funds service and selection. Over time, specialty retail declines. Then, consumers lose variety. Innovation slows because fewer stores support new ideas.

This outcome reflects market structure, not poor execution by liquor stores.

What the next five years likely bring

Grocery chains will keep seeking broader alcohol rights. RTDs and spirits-based beverages will remain a key focus. At the same time, more states will debate guardrails as store counts fall.

Two paths appear likely. Some states will allow limited growth with caps or spacing rules. Others will favor convenience and accept consolidation. Colorado’s recent response suggests lawmakers still see value in specialty retail.

Liquor stores must plan for both outcomes.

Ten ways liquor stores can compete effectively

- Build baskets, not just items. Sell solutions for events and occasions.

- Lead with education. Make recommendations fast and simple.

- Curate deeply. Offer brands grocery chains avoid.

- Protect margin. Match prices only on known staples.

- Strengthen loyalty programs. Reward repeat visits and discovery.

- Rotate discovery displays weekly. Keep the store feeling new.

- Use tastings with purpose. Capture emails and drive repeat sales.

- Negotiate smarter with distributors. Ask for exclusives and training.

- Improve convenience selectively. Add pickup and delivery where legal.

- Act like experts. Publish guides and local rankings consistently.

Why this moment matters

Grocery store alcohol competition reshapes liquor retail at a structural level. The issue goes beyond price. It affects store survival, consumer choice, and craft innovation. Liquor stores that adapt can still win. However, adaptation requires focus, clarity, and discipline.

The next five years will decide whether specialty alcohol retail remains viable in many markets.

Frequently Asked Questions About Grocery Store Alcohol Competition

What is grocery store alcohol competition?

Grocery store alcohol competition refers to grocery chains selling alcohol alongside liquor stores. This expansion increases price pressure on independent retailers.

How does grocery store alcohol competition affect liquor store sales?

Grocery store alcohol competition pulls high-volume national brands into lower-margin channels. As a result, liquor stores lose core revenue and traffic.

Why do grocery stores focus on national alcohol brands?

Grocery chains prioritize fast turnover and simple inventory. National brands offer predictable volume, strong promotions, and easier logistics.

Does grocery store alcohol competition reduce consumer choice?

Yes, consumer choice often narrows over time. Grocery shelves favor fewer brands, while specialty selections lose placement.

How does grocery store alcohol competition impact craft producers?

Craft producers depend on liquor stores for education and discovery. When liquor stores weaken, fewer outlets support new brands.

Are grocery store employees trained to recommend alcohol?

Most grocery staff receive limited alcohol training. Liquor store employees usually provide deeper product knowledge and guidance.

Why do liquor stores feel pressure even when alcohol sales remain strong?

Overall demand can stay stable while sales shift channels. Grocery store alcohol competition changes where revenue flows.

Can liquor stores compete with grocery store alcohol competition?

Yes, liquor stores can compete through service, curation, education, and local engagement. However, price competition alone rarely works.

Will grocery store alcohol competition continue to expand?

Expansion will likely continue in some states. However, policymakers increasingly debate limits after measuring market impact.

Why does grocery store alcohol competition matter for policymakers?

It affects small business survival, consumer choice, and local economies. Long-term effects often emerge years after expansion.